Banks keep our money safe, provide us interest, give us so many advantages – debit card, net banking, cash deposit, cash withdrawal, and the list seems to be endless. But how do banks earn money? What is their source of profit? How do they have so many funds to lend us loans and reward us with interest? Surprisingly, we don’t even pay them for there services except for some mere charges.

Let’s discover… here are a few ways by which banks dig their profits:

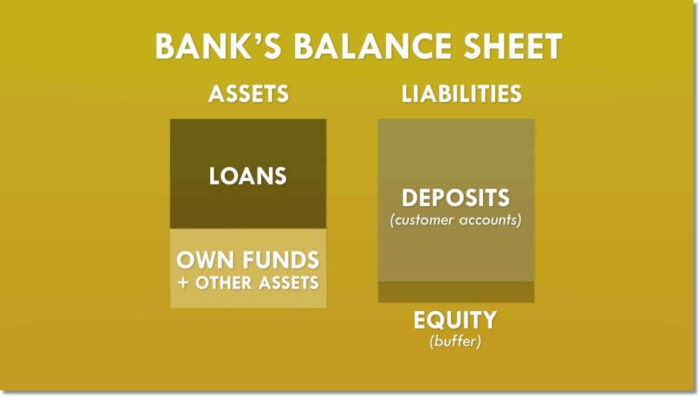

1. Core Deposits

The largest source of income for the banks are deposits. Account holders entrust money to the banks for safekeeping and use in future transactions, as well as modest amounts of interest.

Deposits in which people maintain accounts for years at a time, customers reserve the right to withdraw the full amount at any time. They can withdraw money upon demand and the balances are fully insured and therefore, banks don’t have to pay much for this money.

2. Wholesale Deposits

When a bank is unavailable to deduce sufficient core deposits, the bank can rely on wholesale sources of funds. Honestly speaking, there is nothing wrong in a bank turning to wholesale funds, but investors should consider what it says about a bank when it relies on this funding source.

The higher cost of wholesale funding actually means that a bank either has to settle for a narrower interest spread, and lower profits, or pursue higher yields from its lending and investing, which means taking on greater risk.

3. Share Equity

This is an important part of a bank’s capital. Common equity is that capital of the bank which is raised by selling shares to outside investors. While larger banks often pay dividends on their common shares, there is no requirement for them to do so.

Equity capital is expensive therefore, banks issue shares only when they need to raise funds for an acquisition, or when they need to repair their capital position, typically after a period of elevated bad loans.

4. Debt

Debts are used to smooth out the ups and downs in the funding needs. Debt is usually a much smaller percentage of total deposits or loans at most banks and is, accordingly, not a vital source of loanable funds

5. Loans

Loans are the primary use of funds and an essential way of creating income for banks. Banks make loans with variable or adjustable interest rates and borrowers can often repay loans early, with little or no penalty.

Consumer Lending is another important use of funds. Mortgages are used to buy residences and the homes are kept as security that collateralizes the loan. It is typically written for 30-year repayment periods with a fixed, adjustable, or variable interest rates.

6. Credit Cards

Credit Cards are another significant use of funds. In this, money can be drawn at any time. Credit card lending requires lucrative fees for banks: interchange fees charged to merchants for accepting the card and entering into the transaction, late-payment fees, currency exchange, over-the-limit and other fees for the card user, as well as elevated rates on the balances that credit card users carry, from one month to the next.